Key Takeaways

I. Why Algorithmic Transparency Is An Engineering Problem, Not A Compliance One

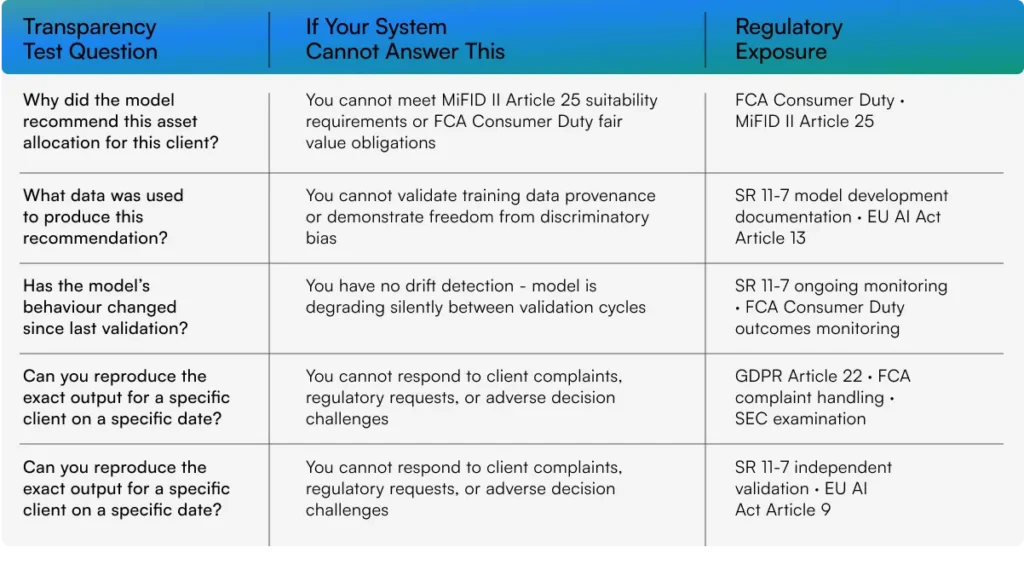

II. The 5-Question Transparency Test: Can Your WealthTech AI Answer These?

III. What Algorithmically Transparent AI Infrastructure Looks Like In Production

IV. Three Questions That Reveal Your WealthTech AI’s Transparency Gap

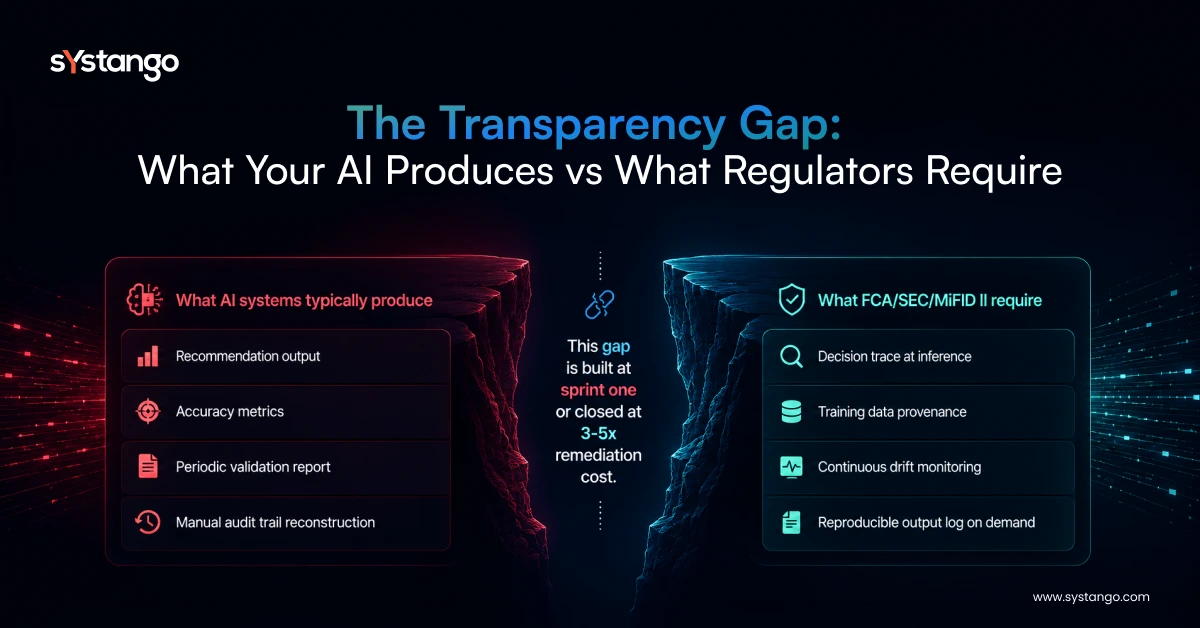

Your wealthtech AI is making investment decisions. Thousands per day. Faster than any human portfolio manager, with more data inputs than any human can process. And when the FCA, the SEC, or a client asks ‘why did the model recommend this?’ — the silence is deafening.

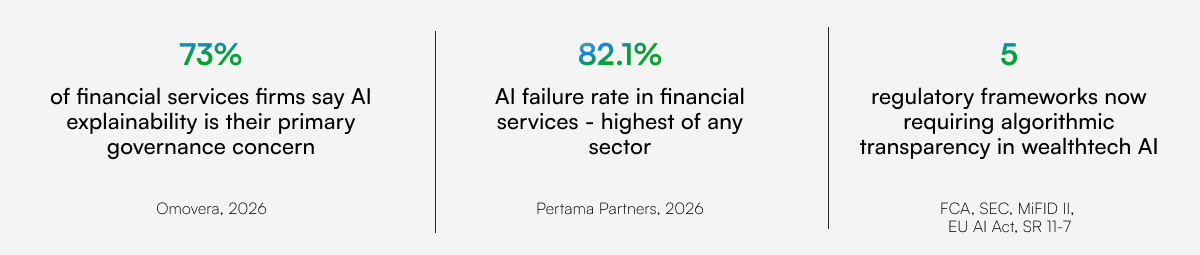

Algorithmic transparency is not a philosophical debate about AI ethics. It is an engineering requirement with specific regulatory deadlines. MiFID II Article 25 requires suitability evidence per recommendation. SR 11-7 requires independent validation documentation. FCA Consumer Duty requires fair value evidence at the point of inference. The EU AI Act, binding across UK-adjacent markets from 2025, requires high-risk AI to produce explanations of its logic on demand. AI governance in wealthtech is not moving towards these requirements. It has already arrived at them.

The question is not whether your AI in wealth management platforms needs to be explainable. It does. The question is whether it was built to be explainable, or whether explainability is an engineering problem that has been deferred to a compliance review that cannot fix it.

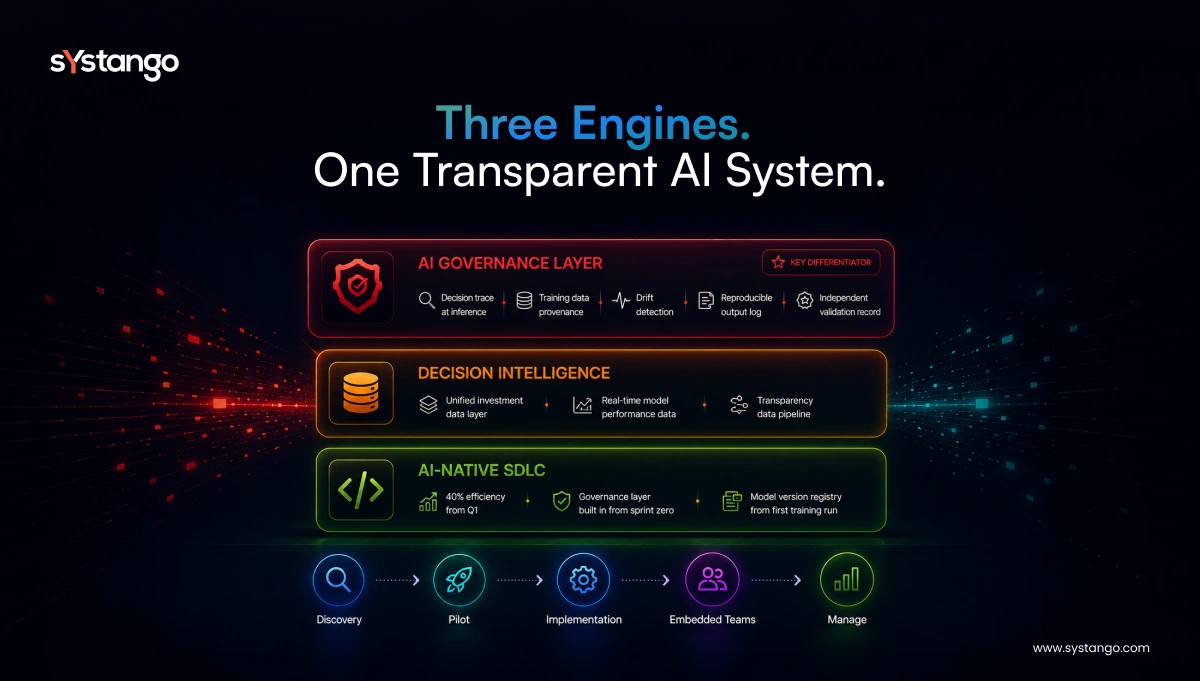

The short answer: Algorithmic transparency in wealthtech AI requires five engineering capabilities: decision traceability at inference, training data provenance, automated drift detection, reproducible output logging, and independent validation records. None of these can be retrofitted after the model is deployed. All five must be present before the model goes into production. The AI Governance Layer is the engineering architecture that produces all five as a byproduct of the build.

I. Why Algorithmic Transparency Is An Engineering Problem, Not A Compliance One

Most AI in investment management teams treat explainability as a compliance deliverable: the compliance team reviews the model after it is built and produces documentation. This is the wrong sequence, and it is expensive to correct.

Explainability documentation cannot be generated retrospectively for a model that was not built to produce it. The audit trail for a recommendation made six months ago does not exist unless the system was instrumented to capture it at the time of inference. The training data provenance for a model updated four sprints ago cannot be reconstructed unless the version registry logged it at training time. The independent validation record for the model currently in production cannot be created unless the validation workstream was structured before the model was built.

This is AI implementation challenges in finance at its most expensive: governance discovered after build costs 2–5× more to implement than governance built in from sprint one. For enterprise AI adoption strategy financial services, the organisations that scale AI fastest are those that treat the governance layer as infrastructure, not documentation. The five-question transparency test below is the engineering specification for that infrastructure.

II. The 5-Question Transparency Test: Can Your WealthTech AI Answer These?

Each question is a regulatory requirement. Each ‘cannot answer’ column describes what happens when the engineering answer is missing. Run this test against your current wealthtech scalability challenges and AI deployment.

III. What Algorithmically Transparent AI Infrastructure Looks Like In Production

The following engagement demonstrates what happens when transparency is built as an engineering requirement – not reviewed as a compliance checkpoint.

Problem: An enterprise investment management platform had AI decision-making embedded across multiple operational workflows. The models were performing. The governance infrastructure did not exist: no decision trace at inference, no training data registry, no drift monitoring, no reproducible output logging. When regulators began requesting algorithmic transparency documentation, the engineering team had no mechanism to produce it.

IV. Three Questions That Reveal Your WealthTech AI’s Transparency Gap

Each question identifies a specific engineering gap. Each gap is a buildable deliverable, if it is on the SDLC roadmap before the model trains.

- Pull the audit trail for your most recent AI recommendation. Not the model’s output. The audit trail, the record of exactly which inputs produced exactly this output, for exactly this client, at exactly this time. If your engineering team cannot produce this record within 24 hours, your AI in wealth management platforms does not meet FCA Consumer Duty complaint handling requirements or MiFID II adverse decision standards.

- Check when your model was last independently validated. Not reviewed by the team that built it. Independently validated, with a separate scope, a separate owner, and a documented independence record. If the validation was performed by the same team that built the model, your SR 11-7 compliance gap is the same as the gap WT-MOFU-2 documented. The difference in Blog 3’s context: the explainability requirements add a fourth component to SR 11-7’s three. A model that cannot explain its decisions cannot be independently validated to the standard regulators now require.

- Ask your engineering team how they would demonstrate ‘no discriminatory bias’ in your AI’s recommendations. The EU AI Act Article 10 requires high-risk AI to use data that is free of discriminatory patterns. The FCA’s Consumer Duty requires fair outcomes across client groups. If the answer is ‘the model was trained on historical data’ without a documented bias testing protocol, neither requirement is met. Knowing how to scale AI in financial services responsibly means building bias testing into the CI/CD pipeline, not addressing it in a compliance document after the model is live.