Key Takeawys

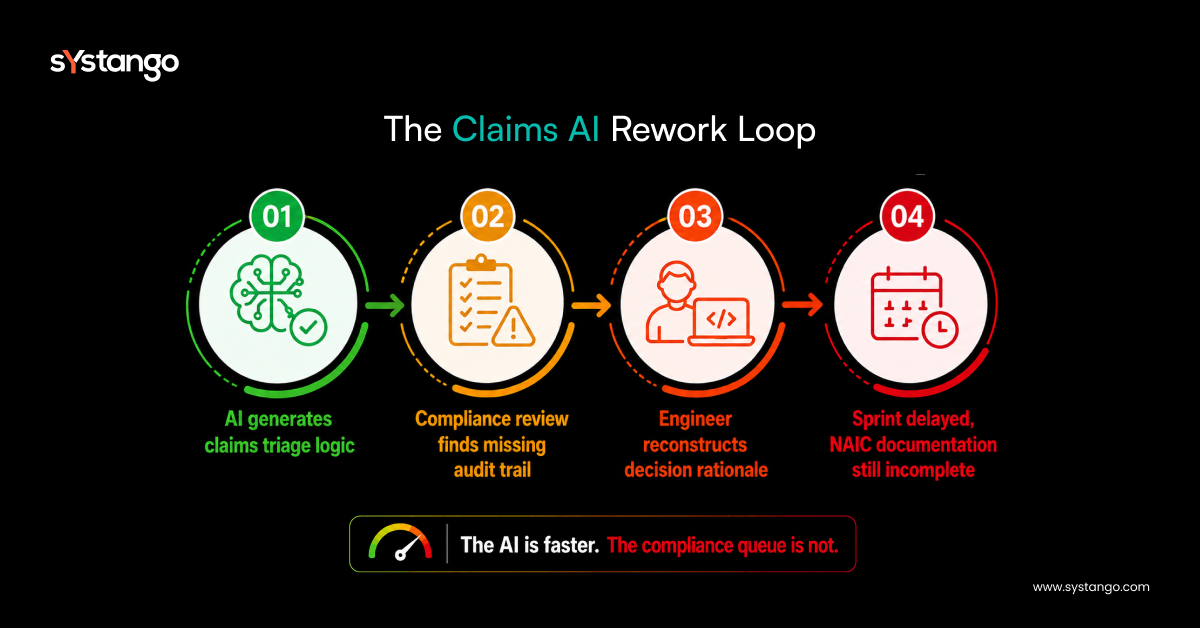

I. The rework loop InsurTech claims teams cannot see in their sprint metrics

II. Three rework patterns draining claims engineering capacity

III. What breaks the claims AI rework loop: governance at every inference

IV. Production monitoring that catches drift before it becomes a compliance event

V. Where AI Workbench delivers in claims automation

VI. Expected outcomes – claims AI without the rework overhead

VII. Why the claims AI governance window is closing in 2026

VIII. Three audits to run on your claims AI this week

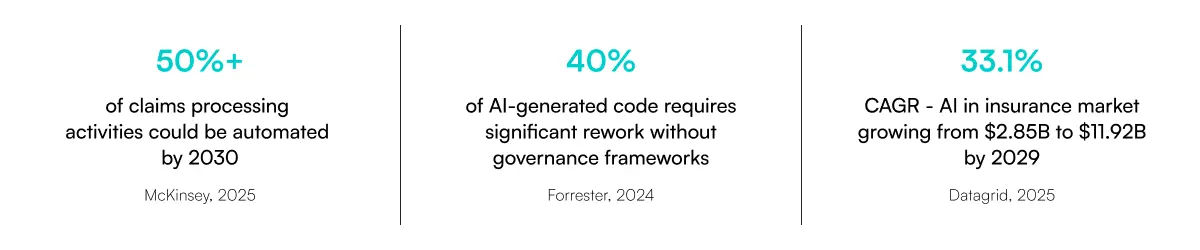

McKinsey’s analysis shows 50%+ of claims processing automation activities could be automated by 2030. What the analysis does not show is the rework queue that builds up before you get there. Claims automation AI without a governance-first AI layer in the SDLC produces code faster than compliance review can process it, generates triage logic without the NAIC AIS Program audit trail, and creates the AI chaos tax in the function that was supposed to benefit most.

Forrester Research found 40% of AI-generated code requires significant rework without governance frameworks. In insurance claims automation, that rework has regulatory weight: under GDPR Article 22, an incorrect triage decision is an explainability failure. Under the NAIC Unfair Claims Settlement Practices Act, it is a potential regulatory breach. This is the task-level AI vs system-level AI problem made costly.

I. The rework loop InsurTech claims teams cannot see in their sprint metrics

AI tools in AI in insurance claims platforms generate triage logic faster than before. But NAIC’s AIS Program requires written governance documentation for each AI claims system. GDPR Article 22 requires each automated decision to be explainable to the policyholder on demand. FCA Consumer Duty requires fair value evidence. None of these are produced by the AI tools generating the triage logic – each is an engineering task the sprint plan did not include.

II. Three rework patterns draining claims engineering capacity

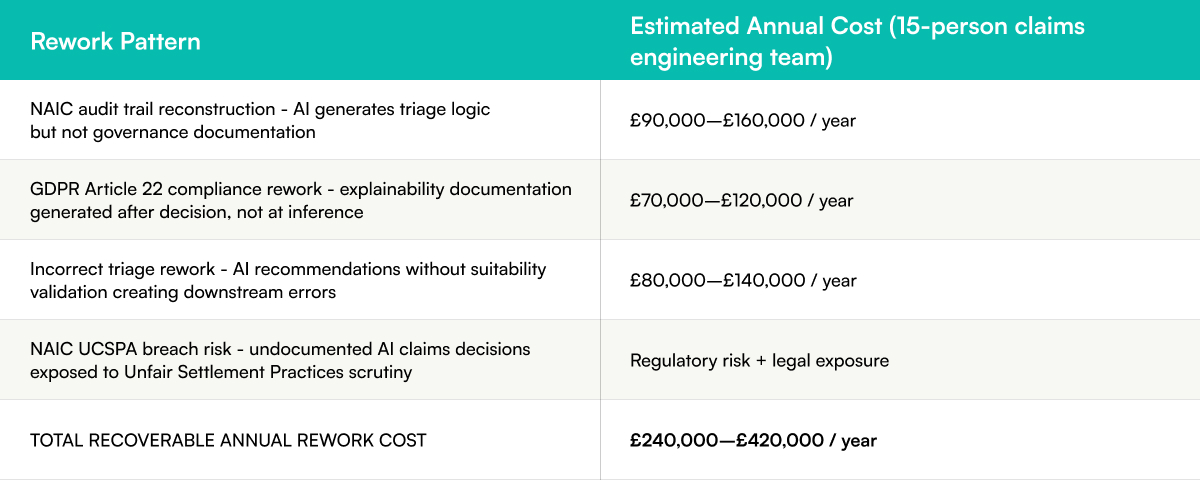

Rework pattern 1 – The governance documentation gap: AI generates triage logic but not AIS Program records

NAIC’s AIS Program requires documentation of governance, risk management, and bias testing for every AI system in claims. AI triage tools generate the logic. They do not generate the written records regulators require. Every sprint that adds AI capability without governance documentation widens the compliance gap.

Rework pattern 2 – The explainability gap: GDPR and NAIC require decisions the AI cannot reconstruct

GDPR Article 22 and the NAIC Unfair Claims Settlement Practices Act both require automated claims decisions to be explainable and auditable on demand. An automated claims processing system that cannot produce the basis for a triage decision cannot meet this requirement. The documentation must be generated at inference time – not reconstructed six weeks later.

Rework pattern 3 – The integration mismatch: claims AI designed for clean data meets production reality

Claims AI models are trained on curated datasets. Production claims data is incomplete, multi-format, and full of edge cases outside training distributions. Without a production monitoring layer detecting drift and triggering revalidation, AI in insurance claims platforms degrade silently between model updates.

III. What breaks the claims AI rework loop: governance at every inference

NAIC and GDPR documentation generated by the AI system – not the compliance team

Claims platforms that have eliminated the rework loop generate NAIC AIS Program records, GDPR Article 22 explainability outputs, and Consumer Duty evidence as first-class outputs of every inference. The compliance reviewer receives a decision with governance documentation already present. The rework queue shrinks because documentation exists before it is requested.

IV. Production monitoring that catches drift before it becomes a compliance event

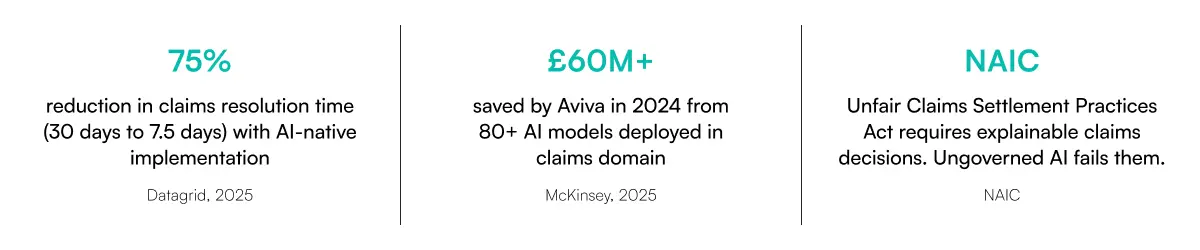

Claims AI platforms that resolve the rework loop embed model drift detection, triage monitoring, and NAIC bias testing into the production layer. Based on Systango’s delivery data, this approach reduces compliance rework rounds from 3.2 to 1.8 per sprint.

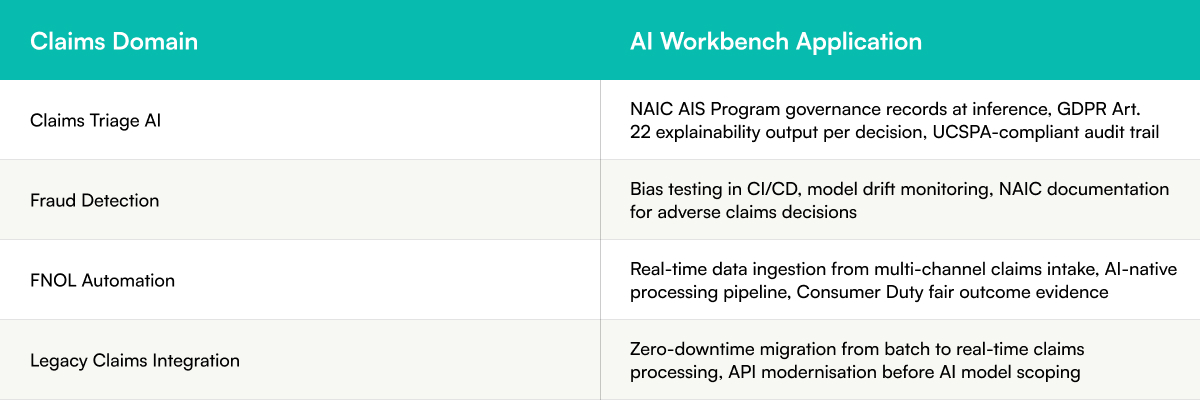

V. Where AI Workbench delivers in claims automation

VI. Expected outcomes – claims AI without the rework overhead

Documented delivery results from live AI Workbench engagements – not projections.

VII. Why the claims AI governance window is closing in 2026

The NAIC Model AI Bulletin is active in 15+ US states, and the EU AI Act’s high-risk provisions are fully applicable from August 2026. GDPR Article 22 enforcement has already generated actions in EU jurisdictions. UK insurers face the same explainability obligations under UK GDPR. Every claims AI sprint without a governance layer is a sprint of widening exposure against standards that are already operative.

VIII. Three audits to run on your claims AI this week

1. Does each AI-assisted claims decision produce NAIC AIS Program records, GDPR Article 22 explainability, and an audit trail at inference time? If the answer is ‘we add that manually,’ calculate reconstruction hours per sprint × engineering rate. That is your recoverable annual rework cost.

2. Does your claims AI have a production monitoring layer detecting drift and triggering revalidation? Without it, triage accuracy degrades silently between model updates.

3. For your last three triage decisions flagged for manual review: was the AI override rationale documented? If not, that is a NAIC UCSPA gap compounding with every undocumented adverse claims decision.

About Systango

Systango is a publicly listed AI-native digital engineering company. We build governance-first AI systems for regulated FinTech, WealthTech, and InsurTech organisations in the UK and US. From funded startups to enterprises including Google and Cisco, we are our customers’ technology partner – AI-native by design, governance-first by principle, outcome-accountable by default.