Key Takeaways

I. What FCA Consumer Duty Actually Requires From WealthTech AI Engineering

II. Why Most WealthTech AI Fails The Consumer Duty Review

III. How A Governance-First SDLC Resolves The Consumer Duty Gap

IV. What Consumer Duty-Compliant AI Delivery Looks Like In Practice

V. Three Questions To Ask About Your WealthTech AI Before The Next FCA Cycle

Your wealthtech platform’s AI model recommended a portfolio reallocation to a client with a moderate risk profile. The FCA’s Consumer Duty outcomes monitoring asks one question: can you demonstrate that the recommendation was in that client’s best interest? Not ‘was it probably fine.’ Can you produce the documented rationale, the suitability alignment evidence, and the audit trail – for that specific recommendation, on demand?

If the answer involves your engineering team reconstructing it from logs, the FCA Consumer Duty AI engineering requirement is not being met. Consumer Duty is not a compliance review at the end of the build. It is an architecture decision made – or missed – at sprint one.

The short answer: FCA Consumer Duty requires wealthtech AI systems to produce suitability evidence, fair value documentation, and explainable outcomes at inference time – not reconstructed after the fact. The AI governance layer in the SDLC is the engineering decision that makes this possible. Built in from sprint one, it costs a fraction of the retrofit. Missed, it costs the platform its deployment.

I. What FCA Consumer Duty Actually Requires From WealthTech AI Engineering

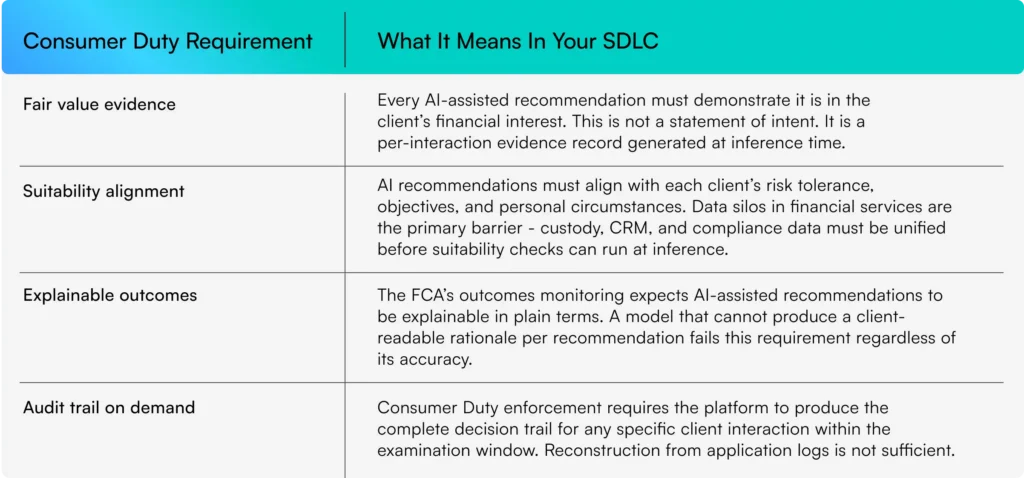

The FCA consumer duty AI engineering wealthtech requirement is not a policy document. It is four specific engineering deliverables that must exist before a wealthtech AI model goes into production. The FCA’s July 2023 Consumer Duty rules, reinforced by the 2024 outcomes monitoring guidance, make each of them operationally mandatory.

Key point: The root cause of AI adoption challenges in financial services in wealthtech is always a sprint one decision missed. None of these four requirements can be retrofitted cleanly: Suitability alignment requires the governance layer to be encoded before the first training run. Explainability requires the model architecture to be designed for interpretability from sprint one. Fair value evidence requires the data layer to be structured for per-interaction output logging before the model sees production data

II. Why Most WealthTech AI Fails The Consumer Duty Review

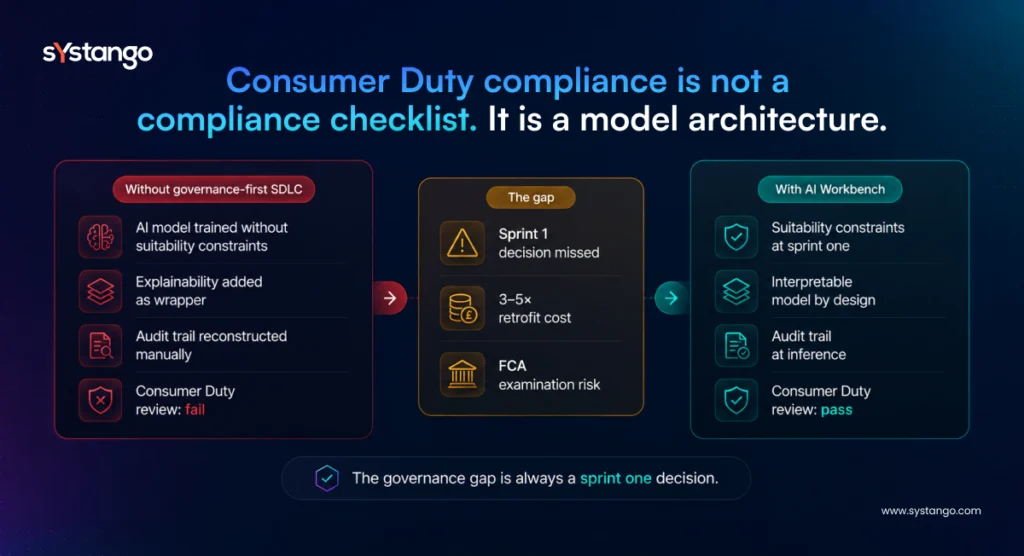

The AI adoption challenges in financial services that produce Consumer Duty failures in wealthtech are not model failures. They are the wealthtech platform challenges of sequencing – building AI capability before the governance layer. They are sequence failures. The fintech legacy system modernization pattern – building the AI capability before the governance layer – is the most common and most expensive mistake in regulated wealthtech engineering.

The retrofit problem

Wealthtech platforms that deploy AI models and subsequently map Consumer Duty requirements to them face a fundamental engineering problem: the model was not designed to produce Consumer Duty evidence. Adding suitability alignment after training requires retraining. Adding explainability after deployment requires rebuilding the inference architecture. The wealth management platform modernization most platforms undergo produces a worse outcome than building correctly from the start.

The data silo problem

Consumer Duty suitability alignment requires the AI model to access each client’s documented risk profile, investment objectives, and interaction history at inference time. For most wealthtech platforms, this data sits across custody, CRM, and compliance systems that were never designed to interoperate. Data silos in financial services are the infrastructure gap that makes Consumer Duty compliance impossible at inference time – not a governance document problem.

The governance-as-overhead problem

Engineering teams that treat Consumer Duty compliance as a project phase – a sign-off stage after the model is built – consistently discover the requirements after the build. Deloitte’s 2024 Financial AI Adoption Report found 60%+ of financial services firms cite compliance requirements discovered after completion as their primary AI delay cause. In wealthtech, the FCA’s Consumer Duty oversight means this delay costs more than time.

III. How A Governance-First SDLC Resolves The Consumer Duty Gap

The wealth management platform modernization approach that resolves the Consumer Duty gap has three non-negotiable characteristics. None involves rewriting the entire platform in a single programme.

The data layer is unified before the model is scoped. Consumer Duty suitability alignment requires the AI model to access each client’s risk profile, investment objectives, and interaction history at inference time. The unified data layer – connecting custody, CRM, portfolio, and compliance systems in real time – is the architectural prerequisite. Platforms that scope the AI model before resolving their data layer build a model that works in the sandbox and fails at the Consumer Duty review.

Governance constraints are encoded before the first training run. FCA consumer duty AI engineering wealthtech requires suitability alignment to be encoded as governance layer constraints that run at inference time – not checked manually after the recommendation is generated. This means the model architecture is designed around Consumer Duty requirements from sprint zero. The alternative is a model that recommends accurately but cannot demonstrate suitability, which is a Consumer Duty failure regardless of the recommendation quality.

Explainability is a model design decision, not a reporting wrapper. Consumer Duty’s requirement for plain-terms explainability requires the model to generate a client-readable rationale as a first-class inference output. Adding explainability after deployment as a summarisation layer on top of a black-box model does not meet this standard. The AI Governance Layer in Systango’s AI Workbench delivery framework implements interpretable model architectures – SHAP values, attention weights, confidence parameters – as engineering deliverables from sprint one, not retrofit options from sprint twelve.

IV. What Consumer Duty-Compliant AI Delivery Looks Like In Practice

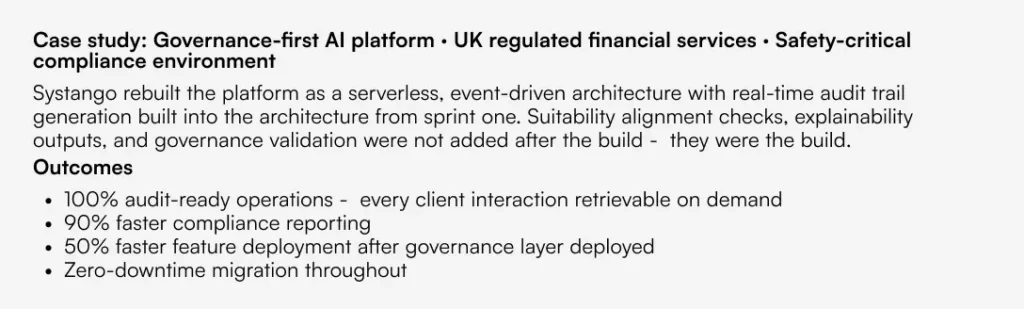

The following engagement demonstrates what happens when the governance layer is built before the model, not after.

Problem:

Legacy systems, fragmented compliance data, and manual workflows created audit trail gaps in a regulatory environment where every certification record and client interaction must be retrievable on demand. The compliance team was reconstructing audit evidence manually before every review cycle.

V. Three Questions To Ask About Your WealthTech AI Before The Next FCA Cycle

Each question identifies a specific Consumer Duty gap in your current platform. Each gap is a buildable engineering deliverable – if it is on the roadmap.

• Can your platform produce suitability alignment evidence for a specific client recommendation from 90 days ago? If the answer requires your engineering or compliance team to reconstruct it manually, your AI governance layer does not meet the Consumer Duty standard. Suitability evidence must be generated at inference time and stored as an immutable event record.

• Is explainability built into your model architecture – or added as a reporting wrapper after the inference? A reporting wrapper that summarises model outputs is not the same as an interpretable model that produces a client-readable rationale at inference. The FCA’s Consumer Duty outcomes monitoring tests the former and requires the latter.

• Did your compliance team review the AI governance requirements before the first model was trained – or after? If compliance reviewed after build, your platform carries the retrofit risk. The AI Workbench delivery framework makes compliance a design partner from sprint zero – the decision that eliminates the Consumer Duty retrofit cost entirely.