Key Takeaways

I. The Legacy Core System Trap: Why The Big-Bang Rewrite Fails Every Time+

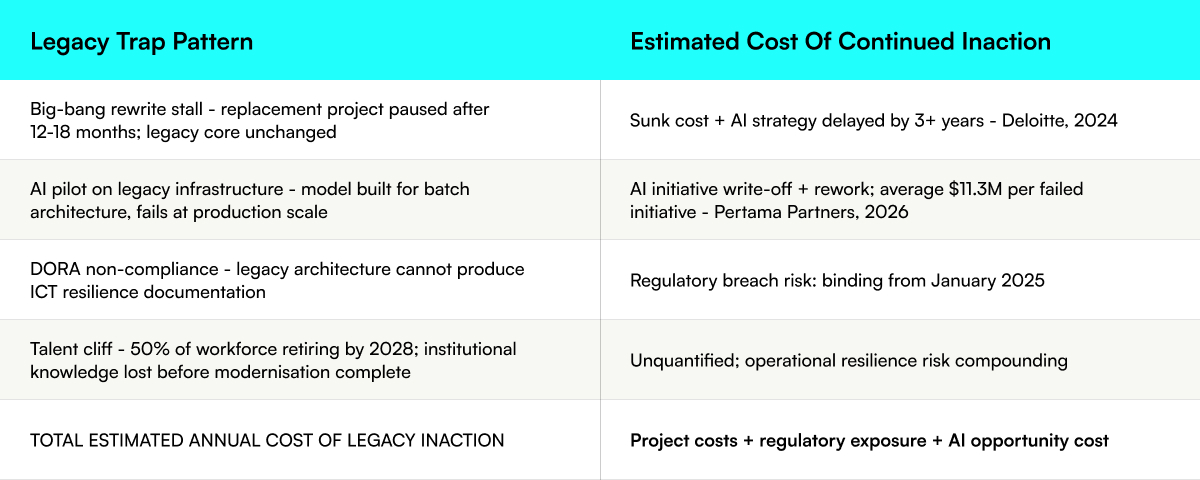

II. Three Patterns That Keep InsurTech Platforms In The Legacy Trap

III. What Breaks The Legacy Trap: Sequenced Decoupling, Not Replacement

IV. Where AI Workbench delivers in InsurTech legacy modernisation

V. Expected Outcomes – InsurTech Legacy Modernisation Without The Big-Bang Risk

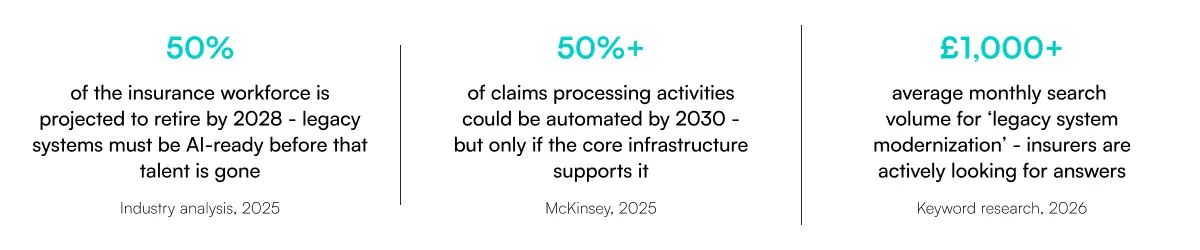

VI. Why the legacy modernisation window is narrowing in 2026

VII. Three diagnostics to run on your legacy core this week

The most expensive insurance technology decision of 2026 is not which AI model to buy. It is when to modernise the legacy core that AI must connect to. Every InsurTech core system modernisation initiative eventually hits the same blocker: the policy admin system was never designed to receive AI inference outputs in real time.

The common response is a 3-year big-bang rewrite – also the most common way to lose three years. The legacy system modernisation approach that works is sequenced decoupling: data layer first, API modernisation second, AI capability third. Based on Systango’s delivery data, clients complete this with zero downtime and 80%–90% infrastructure cost reduction.

I. The Legacy Core System Trap: Why The Big-Bang Rewrite Fails Every Time

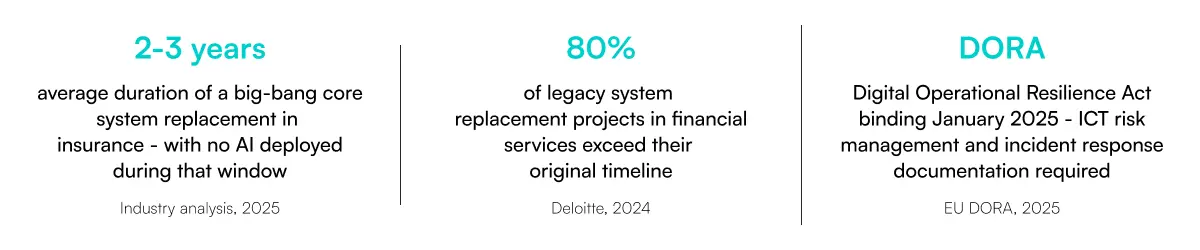

The challenges of legacy systems in InsurTech are consistent: the policy admin core is deeply connected to every workflow, and proposing full replacement triggers a risk assessment that accurately identifies the project as the highest operational risk the organisation faces. The project is approved, delayed, descoped, and eventually paused – legacy core intact, AI strategy waiting. Meanwhile DORA, FCA Consumer Duty, and NAIC’s AIS Program each require governance documentation the legacy environment cannot produce.

II. Three Patterns That Keep InsurTech Platforms In The Legacy Trap

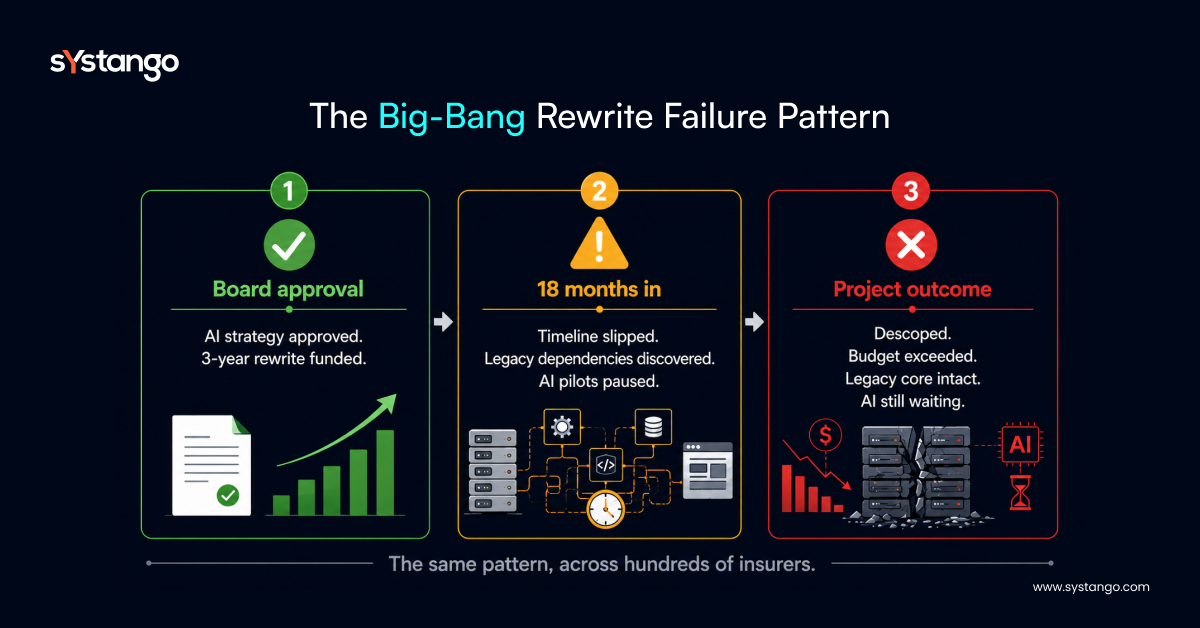

Pattern 1 – The big-bang stall: the project that cannot be abandoned and cannot be completed

A full policy admin system replacement is genuinely high-risk: complex product configurations, regulatory reporting, and multi-decade client data that cannot be cleanly migrated in one programme. The AI chaos tax compounds during the stall – every sprint is a sprint of delayed AI capability and increasing distance from AI-native competitors gaining market share at 33.1% CAGR, per Datagrid.

Pattern 2 – The AI-on-legacy failure: pilots that succeed and deployments that cannot scale

The most common application modernisation mistake in InsurTech is scoping the AI model before resolving the data layer. A claims triage AI trained on clean data will fail when connected to the production policy admin system – which delivers batch data, inconsistent formats, and partial records.

Pattern 3 – The compliance gap: legacy infrastructure cannot carry the AI governance load

DORA, Consumer Duty, and NAIC’s AIS Program all assume the infrastructure hosting AI can produce audit-ready documentation at inference time. Legacy batch-processing architectures were not built to this specification. The compliance requirements do not care when the infrastructure was built. They apply from the date they came into force.

III. What Breaks The Legacy Trap: Sequenced Decoupling, Not Replacement

Data layer first – API modernisation second – AI capability third

The legacy modernisation services approach that works treats the legacy core as a stable data source to be decoupled from, not replaced. Sequence: data layer unification first (real-time API connecting policy admin, claims, and compliance data); API modernisation second (event-driven architecture replacing batch); AI capability third (governance layer already built in). Systango clients complete this sequence with zero production downtime.

The governance layer built before the first model is scoped

Every cloud transformation services engagement for InsurTech AI must include DORA ICT resilience documentation, NAIC AIS Program records, and Consumer Duty explainability as design inputs – not post-build deliverables. Platforms that treat regulatory requirements as architectural constraints eliminate the retrofit cost that destroys most AI-on-legacy projects.

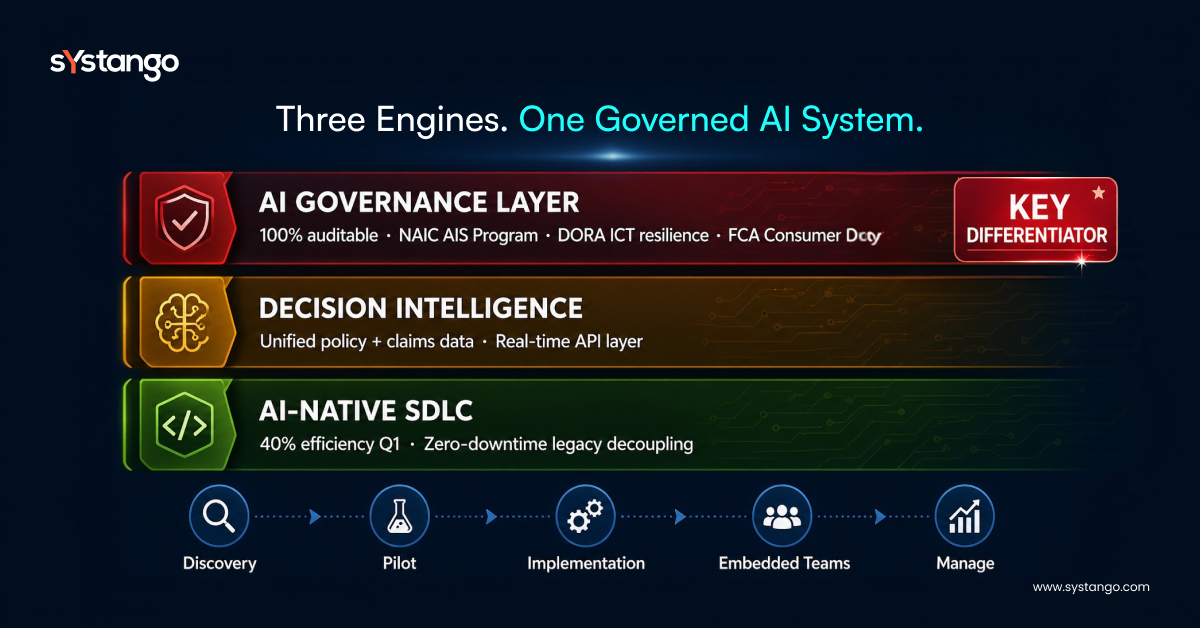

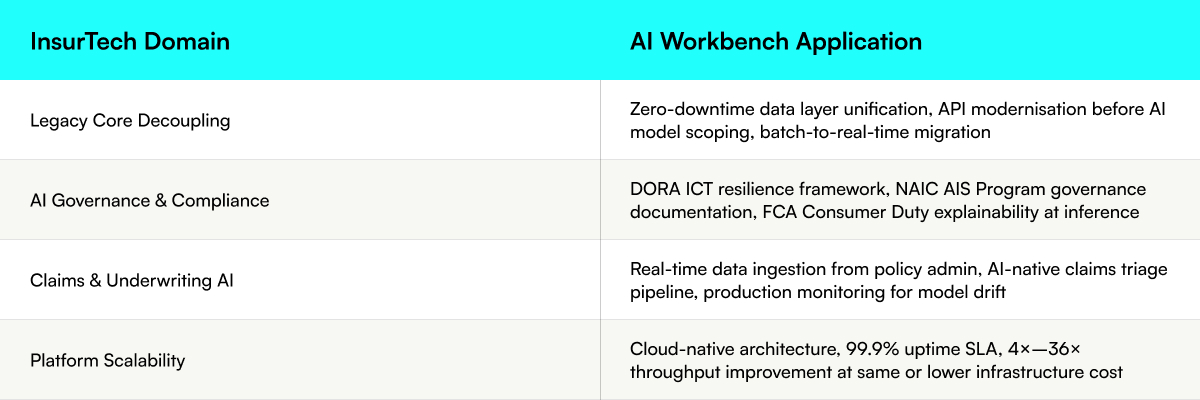

IV. Where AI Workbench delivers in InsurTech legacy modernisation

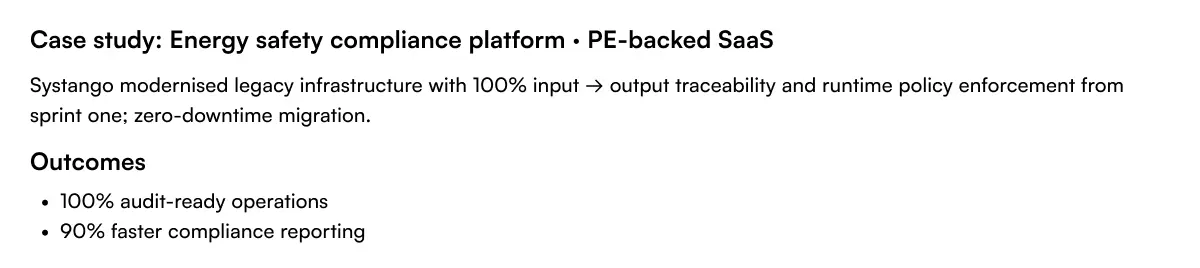

V. Expected Outcomes – InsurTech Legacy Modernisation Without The Big-Bang Risk

Documented delivery results from live AI Workbench engagements – not projections.

VI. Why the legacy modernisation window is narrowing in 2026

DORA’s ICT risk management requirements are binding now. The EU AI Act’s high-risk provisions for insurance underwriting AI are fully applicable from August 2026. FCA Consumer Duty is active. Every quarter of delay accumulates compliance exposure on infrastructure that cannot meet the governance requirements of the AI systems it must host. The AI in insurance market is growing at 33.1% CAGR, per Datagrid – AI-native competitors are capturing the addressable market legacy-bound platforms cannot serve.

VII. Three diagnostics to run on your legacy core this week

1. Map every data source your AI model needs at production scale and document real-time availability for each. Any batch-only source is your first infrastructure gap. The AI model cannot be designed around data it cannot reliably access.

2. Test your policy admin system against DORA’s three ICT resilience requirements: risk management framework, incident response playbook, third-party dependency map. Each gap grows with every AI capability added before it is resolved.

3. Audit your last AI pilot: what blocked it from reaching production – the data layer or the governance documentation? Each root cause maps to a modernisation priority the Legacy Modernisation Assessment structures in 20 minutes.

About Systango

Systango is a publicly listed AI-native digital engineering company. We build governance-first AI systems for regulated FinTech, WealthTech, and InsurTech organisations in the UK and US. From funded startups to enterprises including Google and Cisco, we are our customers’ technology partner – AI-native by design, governance-first by principle, outcome-accountable by default.